Private equity is a passion investment with a difference, observes Paul Sullivan in the NY Times. Unlike art, cars or collectibles, "it is a financial investment, not a tangible asset. You can’t hang it on your wall, park it in your garage or serve it with dinner. But it has a cachet from the past successes of other investors, and the high barrier to entry creates an air of intrigue."

That air of intrigue covers a wide field – vaster than some investors may realize. The Washington Post's David Ignatius has been studying the murder of his friend and colleague Jamal Khashoggi. He finds that some members of the Saudi hit team that killed Khashoggi may have been trained, under U.S. government auspices, by companies owned by affiliates of a major private equity firm. He also notes that an Israeli-founded company noted for its phone-hacking capabilities is now a British private equity holding.

The appeal of private equity, writes Sullivan, is "the promise of exclusive deals, outsize returns and enviable cocktail parties." Some deals, however, may not be appropriate cocktail party conversation.

Sunday, March 31, 2019

Tuesday, March 26, 2019

Two Ways to Wear a Suit Like a CEO

As annual reports for 2018 appear, notice the crumbling of the business dress code. White shirt and tie is giving way to tieless blue shirt.

Pfizer's CEO photo shows him in suit and tie. Ditto for Bank of America's CEO. But AT&T's CEO photo shows that he has joined the tieless, unbuttoned blue-shirt rebellion. So has Citi's.

CEOs of troubled companies, however, need to look as somber and serious as possible. Leaders of GE and Wells Fargo still wear ties.

JPMorgan Chase's report isn't online yet, but Jamie Dimon presumably will appear with tieless blue shirt as he did a year ago.

For traditionalists, worse is yet to come. The disappearing tie, the WSJ suggests, will be followed by the disappearing business suit. Already, shoppers at the Joseph A. Banks store in NYC have to sidle past displays of khakis and jeans and head upstairs in order to find suits.

West Coast techies are to blame, of course. Judging from photo evidence, the only time Apple's Tim Cook wears a suit is when he visits the White House.

The crumbling dress code leaves wealth managers with a serious challenge, Which fashion look will impress the client – Armani or Lululemon?

Pfizer's CEO photo shows him in suit and tie. Ditto for Bank of America's CEO. But AT&T's CEO photo shows that he has joined the tieless, unbuttoned blue-shirt rebellion. So has Citi's.

|

| AT&T's CEO |

CEOs of troubled companies, however, need to look as somber and serious as possible. Leaders of GE and Wells Fargo still wear ties.

JPMorgan Chase's report isn't online yet, but Jamie Dimon presumably will appear with tieless blue shirt as he did a year ago.

For traditionalists, worse is yet to come. The disappearing tie, the WSJ suggests, will be followed by the disappearing business suit. Already, shoppers at the Joseph A. Banks store in NYC have to sidle past displays of khakis and jeans and head upstairs in order to find suits.

West Coast techies are to blame, of course. Judging from photo evidence, the only time Apple's Tim Cook wears a suit is when he visits the White House.

The crumbling dress code leaves wealth managers with a serious challenge, Which fashion look will impress the client – Armani or Lululemon?

Sunday, March 24, 2019

Where‘s Your Teddy Bear Domiciled?

High net worth folks with several homes often strive to avoid being counted as a resident of a high-tax state. Traditionally, that's meant keeping careful count of how many days are spent in said state, and there are apps for that. But as Paul Sullivan reports in his Wealth Matters column, states such as New York and California have become more sophisticated in their efforts to tax the rich.

Days spent in state represent only one of five tests New York applies. "The state also looks at the size and cost of the New York home compared with those in other states, a person’s business and family ties to the state, and a category that looks at where 'near and dear' items are kept."

That last category is popularly known as the teddy bear test.

The new federal income tax cap on SALT deductions has further motivated the rich to flee their domiciles in high tax states. It has also motivated the high-tax states to fight back. In addition to checking for stuffed animals, New York may examine cell phone records and Facebook posts.

From a revenue standpoint the stakes are high. New York gets 46 percent of its income tax take from the top one percent of taxpayers.

Even top one percent New Yorkers who establish domicile elsewhere could be snared by a new proposed revenue raiser: a pied-à-terre tax on second homes worth over $5 million.

|

|

teddy bears, is now domiciled

in New York, at the Public Library.

|

That last category is popularly known as the teddy bear test.

The new federal income tax cap on SALT deductions has further motivated the rich to flee their domiciles in high tax states. It has also motivated the high-tax states to fight back. In addition to checking for stuffed animals, New York may examine cell phone records and Facebook posts.

From a revenue standpoint the stakes are high. New York gets 46 percent of its income tax take from the top one percent of taxpayers.

Even top one percent New Yorkers who establish domicile elsewhere could be snared by a new proposed revenue raiser: a pied-à-terre tax on second homes worth over $5 million.

Saturday, March 16, 2019

The Pioneer Who Discovered Growth Stocks

Long before Jack Bogle, the father of index funds, there was T. Rowe Price, the father of growth investing. He and Bogle are probably the only two investment managers to popularize an entire theory of investing.

Born March 16, 1898, T. Rowe Price was a chemist by training but a stock picker at heart. While working at a brokerage he decided he wanted to sell advice, not stocks. In 1937 he opened his own investment counseling firm, a bold move in those times. Fee-based investment counsel was rare. The seeds of war were sprouting in Asia and in Europe. In the U.S. four years of painful recovery from the Great Depression had relapsed into a new recession.

Somehow, Price survived and prospered, propelled by his belief that he could outperform the market by selecting stocks whose earnings were growing faster than inflation and faster than the general economy.

After World War II ended, high wartime income tax rates lived on. Price's clients wanted to ease their tax burden by moving money into accounts for their children. (In those days Daddy's Little Taxpayers were entitled to their own low tax brackets.) To facilitate small accounts Price started a mutual fund, the T. Rowe Price Growth Stock Fund.

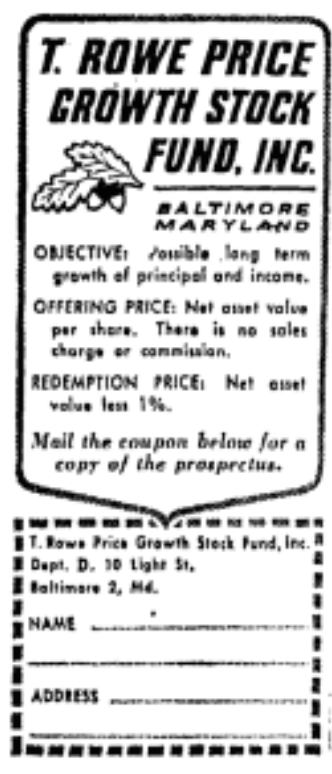

Brokers working on commission didn't sell the Growth Stock Fund. Investors had to buy shares: Send for a prospectus. Fill out the accompanying new-account form. Return it with a check to Price in Maryland. Nevertheless, the fund's performance led to phenomenal success. In the 1970's, when Jack Bogle decided to make his index fund no load, Price's accomplishment must have bolstered his belief that his index fund could flourish without the help of a commissioned sales force.

Brokers working on commission didn't sell the Growth Stock Fund. Investors had to buy shares: Send for a prospectus. Fill out the accompanying new-account form. Return it with a check to Price in Maryland. Nevertheless, the fund's performance led to phenomenal success. In the 1970's, when Jack Bogle decided to make his index fund no load, Price's accomplishment must have bolstered his belief that his index fund could flourish without the help of a commissioned sales force.

|

| T. Rowe Price |

Somehow, Price survived and prospered, propelled by his belief that he could outperform the market by selecting stocks whose earnings were growing faster than inflation and faster than the general economy.

After World War II ended, high wartime income tax rates lived on. Price's clients wanted to ease their tax burden by moving money into accounts for their children. (In those days Daddy's Little Taxpayers were entitled to their own low tax brackets.) To facilitate small accounts Price started a mutual fund, the T. Rowe Price Growth Stock Fund.

Brokers working on commission didn't sell the Growth Stock Fund. Investors had to buy shares: Send for a prospectus. Fill out the accompanying new-account form. Return it with a check to Price in Maryland. Nevertheless, the fund's performance led to phenomenal success. In the 1970's, when Jack Bogle decided to make his index fund no load, Price's accomplishment must have bolstered his belief that his index fund could flourish without the help of a commissioned sales force.

Brokers working on commission didn't sell the Growth Stock Fund. Investors had to buy shares: Send for a prospectus. Fill out the accompanying new-account form. Return it with a check to Price in Maryland. Nevertheless, the fund's performance led to phenomenal success. In the 1970's, when Jack Bogle decided to make his index fund no load, Price's accomplishment must have bolstered his belief that his index fund could flourish without the help of a commissioned sales force.

•

Jack Bogle was a successful author and a beloved commentator on personal investing. If T. Rowe Price did TV interviews or authored op-eds, I must have missed them. He is said to have disliked public speaking. Thirty-six years after his death, his public image may be getting an overdue boost. Wiley is publishing a bio, T. Rowe Price, the Man, the Company and the Investment Philosophy.

Thursday, March 14, 2019

Wednesday, March 13, 2019

Seeing Helps Investors Believe

MarketWatch offers two graphics that investment advisers may want to add to their educational materials.

This one shows how often and how vigorously stock returns go up and down.

A second graphic (a lively GIF) shows the likelihood of stock investors making money over various time periods. Investors holding for 20 years can't lose – at least they never have. But remember, that perfect success rate assumes all dividends are reinvested.

This one shows how often and how vigorously stock returns go up and down.

A second graphic (a lively GIF) shows the likelihood of stock investors making money over various time periods. Investors holding for 20 years can't lose – at least they never have. But remember, that perfect success rate assumes all dividends are reinvested.

Saturday, March 02, 2019

Are Both Hawaiian War Gods Worth Millions?

Unlike regular investments – stocks, ETFs, bonds – alternative investments such as art can be difficult to value. Perhaps that's why they're alternative investments.

Current illustration: doubts about the value of a wooden statue bought at a Christie's auction by billionaire Marc Benioff for about $7.5 million and donated to a Hawaiian museum.

Is Benioff's purchase, at left, the equal of the similar statue in the British Museum at right? Or is it "the sort of thing you see in a tiki bar"?

Current illustration: doubts about the value of a wooden statue bought at a Christie's auction by billionaire Marc Benioff for about $7.5 million and donated to a Hawaiian museum.

Is Benioff's purchase, at left, the equal of the similar statue in the British Museum at right? Or is it "the sort of thing you see in a tiki bar"?

Subscribe to:

Comments (Atom)