"There's a sucker born every minute," said

Phineas T. Barnum. He certainly would have enjoyed the saga of the Bayou funds,

chronicled extensively in today's New York Times.

Sam Israel's investment approach for his Bayou funds is said to have appealed to investors because it was understandable. No fancy swaps, no leveraged bets on toxic tranches of CDOs. Just good, old fashioned short-term trading in stocks that always seemed to work out well.

Was he actually the only person on the planet who could trade stocks for consistent profits month and month and year after year? If so, why wasn't he world famous? Some of the smarter money must have had its doubts all along.

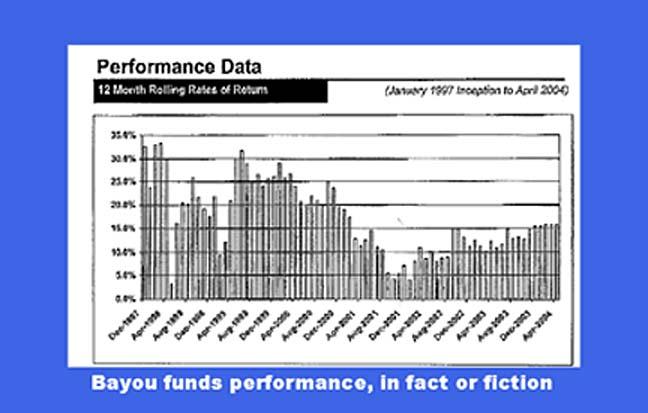

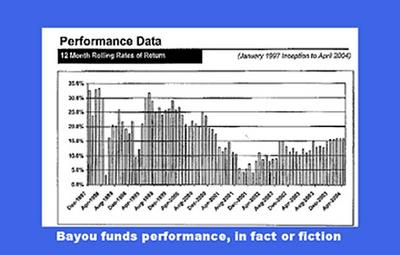

As the chart from Bayou's sales brochure shows, the funds never seemed to have a bad year.

They must have had a really great Sharpe Ratio. Alas, William F. Sharpe himself says his ratio is useless for evaluating the "abolute return" potential of hedge funds. The ratio is too easy to fudge. Sharpe points out that Long-Term Capital Managment had a great Sharpe ratio just before it went bust in 1998. The Bayou funds troubles may have started shortly thereafter.

Bayou's admirable returns, it seems, weren't merely merely fudged, they were imagined. (It helps when your "independent auditor" is your CFO.)

Every affluent investor is a potential sucker. Yet in Bayou's case the biggest sucker of all may have been the manager, Sam Israel III. When his funds’ reported assets were over $400 million, he seems to have been down to $100 million or so. And that sum he supposedly entrusted to a miracle worker to invest in “two private, managed, buy/sell leveraged transactions” that in ten years would turn $100 million into $7.1 billion!

LIke to know what annualized return would be required to achieve that miracle?

Fifty-three percent!

Can regulators protect affluent investors against themselves? It won't be easy. The 100 hedge fund managers of Greenwich, CT, are already

threatening to leave the country if efforts are made to place them under adult supervision.

Looks like responsible wealth managers and trustees will have to try to provide the protection. That won't be easy, either.

Offer too much protection and clients will think you're way too 20th-century fiduciary and take their business elsewhere.

Offer too little and the suddenly-poorer clients will sue the pants off you.

Life

is hard, isn't it?

P. S. According to today's New York Times, Israel told his CFO that the miracle worker had been “referred to us by Alan Greenspan.” Nice touch!