Saturday, May 30, 2009

Madam, Half Your Will Is Missing!

Failure to name a responsible, experienced executor is like having only half a will. So says this 1939 ad from an ancestor of Citi.

Friday, May 29, 2009

SuperSecond Homes: Buy Now?

Bargain Hideways, says Barrons. Those wishing to upgrade their second or third homes may be paying heed:

Bargains? Maybe. But rememember the battle cry of many a major-league baseball team: "Wait 'til next year."

P.S. Better have ten times U.S. Trust's minimum before taking on the expense of a supersecond home.

Real-estate purchase volume among U.S. Trust clients, who have net worths of at least $5 million and investable assets of at least $3 million, increased 60% in March and April over the last two months of 2008, says Jan Reuter, managing director of residential real estate at U.S. Trust, Bank of America's private banking unit. For second homes, volume increased by 200%, she says, "and we are seeing a big increase in inquiries."Examples of bargains that Barron's offers are debatable. Is a nice 8,000 s.f. house on Nantucket, with view, a steal at $7.5 million, down from $8.45 million? What about the megalodge in Big Sky, Montana, at $4.5 million, down from $4.99 million?

Bargains? Maybe. But rememember the battle cry of many a major-league baseball team: "Wait 'til next year."

P.S. Better have ten times U.S. Trust's minimum before taking on the expense of a supersecond home.

Thursday, May 28, 2009

Should non-profits worry about deduction caps?

Earlier this year the President proposed to make a down payment on paying for health care reform by capping the economic value of itemized deductions at 28% for high-income taxpayers. Charities were aghast at the idea, because they know, as the politicians don't, that there will be a behavioral response, that the most of the "revenue enhancement" produced by such a change will be borne by the charities. They know that when pitching high-dollar contributions to the wealthy, they always show the "after tax cost" of making a large donation. The lower the real "cost" of a major donation, the easier the sale is to the rich prospective donor. Capping the value of the deduction reduces the spread, and will make it harder to secure big gifts. Rich people focus on after-tax costs—that's how they got rich in the first place.

Politicians, on the other hand, seem to believe that all philanthropy should be motivated solely by charitable impulses. I suspect that in their world, the charitable deduction itself is pointless, and should be abolished.

The administration is trying to calm the worried charities, reports Tax Notes Today ($).

Yes, the stock market gains since the March lows are impressive. No, I don't think that the wealthy will consider these gains sufficient to cause a spurt in charitable giving. The frame of reference for the wealth effect has to take into account the highs of 2007, not just the recent lows. And it has to take into account the collapse of real estate values as well. I don't buy Mr. Liebman's glib assertion.

Still, two more plausible siren songs were pitched to charities to get them on board at the same Washington, DC meeting. The very real short term benefit to fundraisers of a loss of tax benefits scheduled at a future date (the President wants to begin the cap in the 2011 tax year) is that wealthy taxpayers will undoubtedly accelerate their donations to take advantage of higher tax benefits while they can. Now, suddenly, tax changes do have behavioral effects!

Longer term, nonprofits are being squeezed by health care costs as hard as everyone else. Some $48 billion is spent by nonprofits on health care for their employees, coming in at 4.6% of total expenditures. They would like to see that cost go down—would that be a consequence of a federal takeover of the health care industry?

I dunno—is the cost of buying a new Chrysler vehicle projected to fall dramatically?

The Senate has already passed a resolution rejecting the caps, but that is not likely to be the last word on the subject.

Politicians, on the other hand, seem to believe that all philanthropy should be motivated solely by charitable impulses. I suspect that in their world, the charitable deduction itself is pointless, and should be abolished.

The administration is trying to calm the worried charities, reports Tax Notes Today ($).

Gains in the S&P 500 over the last few months are more than enough to offset the adverse effect that President Obama's 2010 budget proposal might have on charitable giving, said Jeffrey Liebman, executive associate director of the Office of Management and Budget, on May 27.

Yes, the stock market gains since the March lows are impressive. No, I don't think that the wealthy will consider these gains sufficient to cause a spurt in charitable giving. The frame of reference for the wealth effect has to take into account the highs of 2007, not just the recent lows. And it has to take into account the collapse of real estate values as well. I don't buy Mr. Liebman's glib assertion.

Still, two more plausible siren songs were pitched to charities to get them on board at the same Washington, DC meeting. The very real short term benefit to fundraisers of a loss of tax benefits scheduled at a future date (the President wants to begin the cap in the 2011 tax year) is that wealthy taxpayers will undoubtedly accelerate their donations to take advantage of higher tax benefits while they can. Now, suddenly, tax changes do have behavioral effects!

Longer term, nonprofits are being squeezed by health care costs as hard as everyone else. Some $48 billion is spent by nonprofits on health care for their employees, coming in at 4.6% of total expenditures. They would like to see that cost go down—would that be a consequence of a federal takeover of the health care industry?

I dunno—is the cost of buying a new Chrysler vehicle projected to fall dramatically?

The Senate has already passed a resolution rejecting the caps, but that is not likely to be the last word on the subject.

A Wealth Manager For Susan Boyle?

Cheer up, investors, we're just reliving 1973-1982! That popular notion pops up in Alan Steel's piece in the Telegraph. Check out his Scottish firm's web site – comfy and cozier than you would expect from a U.S. asset manager. Alan Steel looks like a firm that would welcome suddenly richer common folk like Susan Boyle.

At Steel's web site, watch his video and "magic number" feature. The marketing lesson? To U.S. ears, even routine thoughts sound better when delivered with a Scots burr.

At Steel's web site, watch his video and "magic number" feature. The marketing lesson? To U.S. ears, even routine thoughts sound better when delivered with a Scots burr.

Wednesday, May 27, 2009

How About VAT?

Once Considered Unthinkable, U.S. Sales Tax Gets Fresh Look, reports The Washington Post.

Prevalent in Europe, a Value-Added Tax could raise big bucks. As the WP chart of projected deficits shows, this country is going to need some very big bucks indeed.

Brooke Astor's Wills: The Boxed Set

Yesterday, The New York Times reports, a massive set of volumes appeared in the court where Brooke Astor's son is on trial:

Was a 2003 codicil, the last Christensen prepared, signed while she was competent?

Could she have been incompetent shortly thereafter, when she signed a codicil prepared by Francis X. Morrissey Jr, the lawyer Astor's son chose to replace Christensen?

Stay tuned.

The putty-colored, tri-level cart stood next to the witness box, its 3-foot-long shelves filled with black binders the size of telephone books. The collection of paperwork represented the sometimes whimsical, sometimes meticulous nature of Brooke Astor. The binders contained more than 30 different wills and amendments to the wills that she executed over half a century.The wills and codicils were entered into evidence as Henry Christensen III, Mrs. Astor's longtime lawyer, took the stand.

Was a 2003 codicil, the last Christensen prepared, signed while she was competent?

Could she have been incompetent shortly thereafter, when she signed a codicil prepared by Francis X. Morrissey Jr, the lawyer Astor's son chose to replace Christensen?

Stay tuned.

Tuesday, May 26, 2009

What Would Benjamin Graham Say?

Sixty years ago this month, the greatest book on investing, Benjamin Graham's The Intelligent Investor, was published. In considerably revised form, it's still in print.

Sixty years ago this month, the greatest book on investing, Benjamin Graham's The Intelligent Investor, was published. In considerably revised form, it's still in print.What would Graham tell today's investors, especially the Boomers whose pensions are threatened, whose 401(k)s are sputtering (whatever happened to employer matches?) and whose overall failure to build financial independence is a national concern?

We'll never know. But if you accept the notion that the present prospect for more bad times, followed by high inflation, is reminiscent of the 1970s, we can guess that Graham might congratulate Boomers on their unexpected stroke of good luck. Jason Zweig in The Wall Street Journal explains:

In the depths of [the 1973-74] crash, near the end of 1974, Mr. Graham gave a speech in which he correctly forecast a period of "many years" in which "stock prices may languish."The bulk of the Boomer generation still has 15 years or more to save and invest before retiring. If they buckle down to the task and stick to their investment guns, they may wind up living higher on the hog than now seems possible.

Then he startled his listeners by pointing out this was good news, not bad: "The true investor would be pleased, rather than discouraged, at the prospect of investing his new savings on very satisfactory terms." Mr. Graham added a more startling note: Investors would be "enviably fortunate" to benefit from the "advantages" of a long bear market.

And maybe some will. But Graham himself recognized that most won't. Few of us possess the "firmness of character" to escape the fears and fads of the day.

Perhaps that's the test of a truly great investment adviser: How many clients' characters can he or she firm up?

Trouble For Self-Paying Insurance Policies?

"Using life insurance to cover the death tax is common practice," reports Arden Dale in the WSJ, "but the strategy is blowing up some estate plans now."

Problems stem largely from expectations about how well investments in a policy will perform. A policy may have been set up to self-pay premiums, based on the notion that investments will beat the interest rate used. Money then builds up and pays the premiums automatically.I haven't the foggiest idea of how this "perpetual motion" approach to life insurance works. Few people do, according to Dale. The possibly endangered policies "are complicated enough that an estate planner or attorney may not feel comfortable vetting them."

But if interest rates decline over time, trouble can occur. The owner may not be aware that the policy is taking out internal loans to keep up with the premium payments.

Wall Street Must Be All A-Twitter

NYT columnist David Brooks may have reached the age of thinning hair, but he's stil capable of planting tongue firmly in cheek. Wall Streeters (and Wall Street types nationwide) must be busy texting and tweeting their favorite zingers from And The Angels Rejoice.

Sample:

Sample:

I’ve been incredibly moved over the past few weeks to watch squads of corporate executives come to the White House so President Obama could announce that he was giving away their money.***

These events have heralded a new era of partnership between the White House and private companies, one that calls to mind the wonderful partnership Germany formed with France and the Low Countries at the start of World War II.

Friday, May 22, 2009

Powers of Attorney

Vanishing financial institutions, Ponzi wannabes, differing state laws…agents acting under durable powers of attorney don't always have it easy. One example offered in this NYT overview:

Wendy S. Goffe, a lawyer… relied on a power of attorney that her husband, Scott Schrum, had given her to piece together his paperless financial life after it was found that he had cancer. While he was disabled, the form gave Ms. Goffe access to electronic records, including those for her husband’s rollover I.R.A. and 401(k) and the 529 college savings plan he had managed for their daughter Maya, 7.

The biggest chore was tracking down shares of stock that Mr. Schrum, also a lawyer, had purchased by exercising employee options online. Because of “a string of bad luck,” Ms. Goffe said, the financial institution holding the options and the couple’s brokerage company had been sold, their Web sites eliminated and the records put into storage. The shares, worth $7,500, had been credited to a stranger’s account.

Wednesday, May 20, 2009

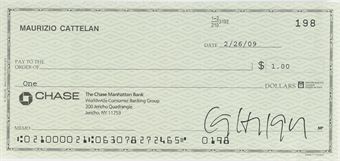

The Art of Checkwriting

This $1 check from Italian artist Maurizio Cattelan sold for about $13,000 – way over the pre-sale estimate – at a Christie's auction of contemporary art in Amsterdam.

Back story: The items presented for sale were especially commissioned works on the subject of "Take the money and run." Whether Bernie Madoff served as honorary auctioneer in absentia is not reported.

Tuesday, May 19, 2009

Money Magazine Features Trust Planning

Though its readers' fortunes may have dwindled, Money magazine reportedly aspires to move upscale. Reflecting that aspiration, Rethinking Your Estate Plan features strategies popular with multimillionaires, including bypass trusts, GRATs and CRTs.

Monday, May 18, 2009

States and Taxes

Arthur Laffer and Stephen Moore in today's WSJ report on their study of low-tax states and high-tax states. Low-tax states fare better, they find. One reason: Americans know how to use the moving van to escape high taxes.

Note: Laffer and Moore are technically incorrect to list New Hampshire among states that lack an income tax. New Hampshire is a great place to work because it does not tax wages. New Hampshire is not such a great place to retire (though lots of us have done so anyway) because it does tax dividend and interest income.

Note: Laffer and Moore are technically incorrect to list New Hampshire among states that lack an income tax. New Hampshire is a great place to work because it does not tax wages. New Hampshire is not such a great place to retire (though lots of us have done so anyway) because it does tax dividend and interest income.

Zombies, Hedge Funds and The Goddess of Debt Reduction

Did you know the term "zombie bank" may date back to 1987, when it was used in connection with the S&L crisis? Do you agree with Naill Ferguson that "human psychology and the failure of most educational institutions to teach financial history" should be blamed for the credit crunch and Great Recession? Does Suze Orman look glamorous reclining by the sea at her Florida home?

As regular readers of the Sunday NYT already know, all these matters and more are covered in what normally might have been the Money Issue of the NYT Sunday Magazine. In the spirit of the times, this year it's called the Debt Issue.

Do you agree with Ferguson that pension funds were lucky to be able to start investing in hedge funds? How about private equity?

As regular readers of the Sunday NYT already know, all these matters and more are covered in what normally might have been the Money Issue of the NYT Sunday Magazine. In the spirit of the times, this year it's called the Debt Issue.

Do you agree with Ferguson that pension funds were lucky to be able to start investing in hedge funds? How about private equity?

Friday, May 15, 2009

Financial Leadership the Old-Fashioned Way

In Al Gordon, Wall Street Legend, we referred to the era when Wall Street made money the old-fashioned way. In his tribute to Gorden in Business Week, Jeffrey Sonnenfeld picks up on the theme. Sonnenfeld also reminds us what a different country this was when Gordon arrived in it:

Born the year President McKinley was assassinated, when there were only 1,500 cars on the road—and before Chrysler, Ford (F), or GM (GM) existed—Gordon knew Civil War generals as a child. He worked with financial legends of another age, such as J.P. Morgan Jr., Robert Lehman, Mortimer Schiff, and Sidney Weinberg, but also knew today's legends, including Jamie Dimon and Steve Schwarzman.

Wednesday, May 13, 2009

The Grandest, Saddest World's Fair

Grandest since the great Columbian Exposition at least, the World's Fair that opened in New York 70 years ago this spring was also the saddest.

Grandest since the great Columbian Exposition at least, the World's Fair that opened in New York 70 years ago this spring was also the saddest.Bright, white and oh so modern, the fair gave Depression-weary Americans a glimpse of a future full of delights. Television! Interstate highways! Automobiles that looked straight out of Buck Rogers!

Yet fair-goers sensed that the future they glimpsed was a mirage, destined to disappear in the horrors of a second World War.

This Fiduciary Trust ad strove to strike a positive tone nonetheless:

Why Governments Shouldn’t Run Banks

Because the government will bring political pressure to bear on lending decisions, which will result in worse decisions, says Executive Suite Blog at NYTimes.com. The last American maker of men's suits, Hart Shaffner and Mark, will have to be liquidated unless Wells Fargo kicks in some more money, which the union and one Congressman are demanding. Although there is no prospect that the money will ever be repaid, that doesn't matter, say the demanders, because Well Fargo took TARP money.

The surprise here is that the NYTimes is reporting this story, not that it's happening. Perhaps they are a tad less pro-union given the ongoing problems with the Boston Globe?

The surprise here is that the NYTimes is reporting this story, not that it's happening. Perhaps they are a tad less pro-union given the ongoing problems with the Boston Globe?

Tuesday, May 12, 2009

Fine print on the Obama estate tax proposals

JLM issued a flash on Obama's estate tax proposal here. In the comments, I expressed skepticism about the revenue scoring, and it turns out there is more to the story.

The first item is indeed to require consistency in estate, gift and income tax reporting, which I don't see as a change from current law. However, there will be new reporting requirements, which should make enforcement more consistent. However, this piece only raises $1.87 billion over ten years. Even that seems high.

More significant, the third item would impose a ten-year minimum term for a Grantor Retained Annuity Trust. Treasury wants to "crack down" on two-year zeroed-out GRATs, which are ways to play the transfer tax lottery without risk. A ten-year term definitely would put a survival risk into the equation. This proposal raises $3.25 billion over ten years. I still wonder how they develop that number—presumably it's the new estate tax revenue because GRATs no longer will be created?

But the real money is in the second item on the list, at more than $19 billion over ten years. We already have in the tax code IRC §2701 to 2704 to prevent the claiming of valuation discounts for certain intrafamily transfers. However, the Treasury reports that wiley taxpayers have figured out ways around these restrictions, so a new group would be added. The proposal would create a whole new category of restrictions to be ignored in valuing an interest in a family-controlled entity. Appropriately, they will be called "disregarded restrictions."

Family Limited Partnerships are the target of this change.

The President's budget also freezes the 45% tax rate and $3.5 million exemption of 2009. Somehow, that freeze will cost $483 million in 2009! How can that be? The freeze gains a scant $3 billion in 2010, the year when there was to be no federal estate tax at all. Seems way low. Then the freeze starts to lose big money, because it is compared to the return to the $1 million exemption and 55% top rate of the Clinton years. In 2015, for example, this change will cost $24.8 billion! That is, just the lost federal estate tax on amounts between $1 million and $3.5 million, plus the additional 10 points on the top rate, will in that year be more than 7 times the entire estate tax collected in 2010!

The Obama administration must be expecting a great many deaths of very rich people that year.

The first item is indeed to require consistency in estate, gift and income tax reporting, which I don't see as a change from current law. However, there will be new reporting requirements, which should make enforcement more consistent. However, this piece only raises $1.87 billion over ten years. Even that seems high.

More significant, the third item would impose a ten-year minimum term for a Grantor Retained Annuity Trust. Treasury wants to "crack down" on two-year zeroed-out GRATs, which are ways to play the transfer tax lottery without risk. A ten-year term definitely would put a survival risk into the equation. This proposal raises $3.25 billion over ten years. I still wonder how they develop that number—presumably it's the new estate tax revenue because GRATs no longer will be created?

But the real money is in the second item on the list, at more than $19 billion over ten years. We already have in the tax code IRC §2701 to 2704 to prevent the claiming of valuation discounts for certain intrafamily transfers. However, the Treasury reports that wiley taxpayers have figured out ways around these restrictions, so a new group would be added. The proposal would create a whole new category of restrictions to be ignored in valuing an interest in a family-controlled entity. Appropriately, they will be called "disregarded restrictions."

Family Limited Partnerships are the target of this change.

The President's budget also freezes the 45% tax rate and $3.5 million exemption of 2009. Somehow, that freeze will cost $483 million in 2009! How can that be? The freeze gains a scant $3 billion in 2010, the year when there was to be no federal estate tax at all. Seems way low. Then the freeze starts to lose big money, because it is compared to the return to the $1 million exemption and 55% top rate of the Clinton years. In 2015, for example, this change will cost $24.8 billion! That is, just the lost federal estate tax on amounts between $1 million and $3.5 million, plus the additional 10 points on the top rate, will in that year be more than 7 times the entire estate tax collected in 2010!

The Obama administration must be expecting a great many deaths of very rich people that year.

Needed: A New Name For Huge, Sickly Banks

Community banks, the dull side of banking, receive front-page attention in today's New York Times.

New deposits and new customers keep trickling in at these safe-and-sane institutions. For some of them, that spells opportunity to gain new trust and investment business as well. But as David Segal writes in his Times article, community banks have an identity problem:

New deposits and new customers keep trickling in at these safe-and-sane institutions. For some of them, that spells opportunity to gain new trust and investment business as well. But as David Segal writes in his Times article, community banks have an identity problem:

[T]he public, politicians and the media have made little distinction between the stress-tested behemoths and the 7,630 community banks across the country — the vast majority of which have watched the crisis like bystanders at a 10-car pileup.What we need is a term to distinguish giant, high-toxicity "banks" from the real and healthy banks. "Blankety-banks'? No, there's got to be a better word or phrase. Ideas, anyone?

Monday, May 11, 2009

Likely bad news for the economy

Administration Plans Tougher Antitrust Action - NYTimes.com

The central paradox:

The Bush administration was slow to substitute the judgment of bureaucrats for that of the market, and the Obama administration is unhappy with that "hands off" approach. Well, as even the Times acknowledges, it's a great day for lawyers.

The central paradox:

It is not unlawful for a company to gain control of a market. It becomes unlawful if the company engages in conduct to exclude or harm competitors with no business justification.Hmmm. I don't suppose that the NYTimes would consider profit maximization a business justification?

The Bush administration was slow to substitute the judgment of bureaucrats for that of the market, and the Obama administration is unhappy with that "hands off" approach. Well, as even the Times acknowledges, it's a great day for lawyers.

Saturday, May 09, 2009

Investing: Mother Knows Best

A photo in The New York Times caught my eye the other day. It showed financial movers and shakers listening to a presentation at The Federal Reserve Bank of New York. Three women sat together up front. One or two more women (it was hard to see) might have been sitting further back. Otherwise, the audience was men in suits. Almost all, men in suits.

Whoa! Wasn't it men in suits who got us into this mess? Wouldn't the financial future look brighter if we saw a Fed audience of women, with maybe a couple of men in suits huddled up front?

It well might. Read Ron Lieber's salute to the superior emotional stability of mothers and other females.

Whoa! Wasn't it men in suits who got us into this mess? Wouldn't the financial future look brighter if we saw a Fed audience of women, with maybe a couple of men in suits huddled up front?

It well might. Read Ron Lieber's salute to the superior emotional stability of mothers and other females.

Photo via Wikimedia Commons

New Tax Hike For Estates?

Tax Boost Proposed for Estates, announces The Wall Street Journal. Turns out to refer not to a hike in federal estate tax rates but to a potential loophole closing:

Tax Boost Proposed for Estates, announces The Wall Street Journal. Turns out to refer not to a hike in federal estate tax rates but to a potential loophole closing:The provision regarding estates would prevent taxpayers from using two different valuations for the same items. Under current law, the White House official said, some people estimate a particular inherited item at one value for the purposes of the estate tax, but estimate the value of the same item at a higher amount when reporting it as a gift.This gambit must be popular. Closing the loophole, according to the Obama administration, would raise an estimated $24 billion over 10 years.

That is because the incentive is to undervalue items when paying the estate tax. But the incentive is to overvalue them when reporting gifts, so that the basis will be higher when calculating capital gains if the item is sold. Under the proposal, taxpayers would have to use the same value for both purposes.

There is, of course, another way to eliminate the loophole, the method proposed by Douglas Holtz-Eakin, a former director of the Congressional Budget Office: Kill the "Death Tax."

Friday, May 08, 2009

Al Gordon, Wall Street Legend

As a kid with a summer job at Kidder Peabody over half a century ago, I didn't see much of Al Gordon. But I do remember him as an impressive, down-to-earth guy. Gordon, who started his Wall Street career in 1925 and started running marathons in his 80s, was Harvard's oldest living graduate. He died May 1 at the age of 107.

Gordon came from an era when Wall Street made money the old fashioned way. Wonder what he thought of the recent crop of financial CEOs and their supersized paydays? Probably not much, judging from this anecdote Douglas Martin includes in Gordon's obituary:

Gordon came from an era when Wall Street made money the old fashioned way. Wonder what he thought of the recent crop of financial CEOs and their supersized paydays? Probably not much, judging from this anecdote Douglas Martin includes in Gordon's obituary:

"What is the food like up there?" it read.… Mr. Gordon offered cash rewards to employees who quit smoking. He always flew economy, and when he noticed a young Kidder vice president sitting in first class, Financial News reported in 2001, he penciled a note for a flight attendant to pass on.

The Great Recession? Good As Over!

Ignore the preceding post. Newly inspired, Boomers are about to launch lucrative second or third careers, achieve unheard of savings rates and make the 2010s a decade for the economic record books.

Their inspiration? The new Star Trek film, an origin story that receives rave reviews from, among others, the NY Times and Washington Post.

The Post's Ann Hornaday:

Their inspiration? The new Star Trek film, an origin story that receives rave reviews from, among others, the NY Times and Washington Post.

The Post's Ann Hornaday:

The marketing campaign for the movie has suggested this is "not your dad's 'Star Trek.' " That's wrong -- no middle-aged Trekkie will be able to hold back tears when the Enterprise first comes into view.Yes, reinvigorated by the myth they grew up with, Boomers will go where no generation has gone before. Some how, some way, and with a little help from their wealth managers, they will Live Long and Prosper.

Thursday, May 07, 2009

Retirement Time Bomb?

One out of two Boomers can't do simple math (divide $2 million by five). And financial illiteracy is the least of their retirement problems.

One out of two Boomers can't do simple math (divide $2 million by five). And financial illiteracy is the least of their retirement problems.One out of two Boomers has no employer retirement plan. Many have little money put aside elsewhere. Much Boomer wealth, such as it was, consisted of home equity (remember that?). For additional depressing findings, see David Ignatius: Boomers going bust.

Why Many Millionaires Don't Feel Wealthy

From Fidelity's new study of millionaire households:

At least Fidelity could find more than 1,000 millionaire households to survey. What's more, those "millionaire households" were defined narrowly, excluding 401(k)s and other employer retirement schemes. Apparently investment real estate was excluded as well.

Even so, most of the households Fidelity surveyed aren't rich. Rich requires $20 million, $30 million or more, depending on who you ask and where you live. As Robert Frank suggests in The Wealth Report, feeling "wealthy" may be more a matter of choice.

[N]early half (46%) of millionaires do not feel wealthy, more than twice as many compared to last year's survey (19%). This is likely due to the fact that millionaires have seen dramatic declines across their holdings.I think Fidelity is on to something.

At least Fidelity could find more than 1,000 millionaire households to survey. What's more, those "millionaire households" were defined narrowly, excluding 401(k)s and other employer retirement schemes. Apparently investment real estate was excluded as well.

Even so, most of the households Fidelity surveyed aren't rich. Rich requires $20 million, $30 million or more, depending on who you ask and where you live. As Robert Frank suggests in The Wealth Report, feeling "wealthy" may be more a matter of choice.

•

Commercial: The Fidelity study finds that hard times have caused millionaires to thirst for financial information. Merrill Anderson's newsletters can help quench that thirst.

Wednesday, May 06, 2009

Look closer

I printed out the jpeg that JLM posted of The Boston Post front page breaking the news that Ponzi was a fraud. How ironic is it that on the page where it is revealed that the promised 50% returns in 45 days would never be fulfilled there are at least half a dozen ads from financial institutions promising 5%, or as much as 5 1/2%, per year? Institutions with names like:

• Hanover Trust CompanyWhat a quaint era it was.

• The Old South Trust Company

• Fidelity Trust Company

• Metropolitan Trust Company

• Tremont Trust Company

• Cosmopolitan Trust Company

Wealth Managers, Rev Your Marketing Engines!

The financial economy is "resetting" and wealthholders are worried. Great time to advertise your wealth-management services!

The financial economy is "resetting" and wealthholders are worried. Great time to advertise your wealth-management services!Rockefeller and Company, the one-time family office, knows that. Haven't seen much adverising from them, but this morning their ad in The New York Times (click for larger image) popped out at me.

Rockefeller and Co. has a simple web site. Check out their straightforward investment review for the first quarter of '09.

Free plug: For investment advisers serving the national or northeastern market, the NY Times is a great place to advertise right now, simply because so much of the Times' usual advertising has dried up. Run an ad and it will be noticed.

Tuesday, May 05, 2009

How Ponzi’s PR Guy Blew The Whistle

Recommended reading and viewing: The New York Times story and slide show on the original Charles Ponzi, inspired by an unpublished memoir by William McMasters, a Boston press agent whose clients incuded JFK's grandfather, Calvin Coolidge and – briefly – Ponzi.

McMasters wrote in his memoir: “I do not anticipate that another Charles Ponzi will ever appear in the financial world.” Bad guess!

McMasters wrote in his memoir: “I do not anticipate that another Charles Ponzi will ever appear in the financial world.” Bad guess!

Monday, May 04, 2009

Three Well-Funded Trusts . . . and Love

An 82-year-old Washington, D. C. widower with 10 children and 47 grandchildren and great grandchildren has won a Powerball cash payout of $79.6 million. To receive the cash he has set up a corporation and three trusts: one for education of the younger generations, another to provide family health care and the third to make gifts to charities.

[David Wilmot, the winner's lawyer] said often when families suddenly come into large sums of money that "it's intense and acrimonious. In this case . . . All I have seen at this point is love."

Jack Kemp, RIP

Jack Kemp was a hero of mine. He was one of the great ones.

I had not heard of Jack Kemp when I joined my wife and others to attend a late-1970s Washington DC rally sponsored by, I think, the Baltic American Freedom League. If it wasn't them, it was some other consortium of advocates for what were then still known as the "captive nations," Lithuania, Latvia and Estonia. Four politicians spoke at the event. The most famous one, whose name I've nevertheless forgotten (but then he was the "star" attraction), talked about the plight of Soviet Jews, which was a bit tangential. Two others provided generic stump speeches. One guy had done his homework, and addressed the crowd as if he really knew them, and shared their very real concerns. This guy was obviously smart, hard working, and deeply respectful of his audience.

This guy was Jack Kemp.

Over the years I accompanied my wife to many small gatherings, and a few large ones, where politicians spoke. They were usually polite, cordial and clueless. Jack Kemp was different.

Here's the New York Times obit on Kemp. It gives him great credit, as it should, for advocating the Kemp-Roth tax cuts.

Here's additional background from Jeffrey Bell on the debates within the Republican party over the Kemp-Roth approach. I had not realized that this had ever been controversial. Even more, I had not realized that Congress passed a diluted version Kemp-Roth tax cuts in 1978, only to have them vetoed by President Carter! Imagine how different the world would be had Carter launched the recovery of capitalism instead of Reagan!

The Kemp-Roth tax cuts were incorporated into the Economic Recovery Tax Act, which was enacted about 20 months after I joined the Merrill Anderson Company. We did very well publishing information for trust departments to use in publicizing the big and small changes that were ushered in. (Before ERTA, a Q-TIP was a just a stick with a cotton ball on the end.) It may have been my work on communicating about ERTA that led Merrill Anderson's senior management to believe I had to potential to break out of our attorney programs.

Thank you, Jack Kemp!

I had not heard of Jack Kemp when I joined my wife and others to attend a late-1970s Washington DC rally sponsored by, I think, the Baltic American Freedom League. If it wasn't them, it was some other consortium of advocates for what were then still known as the "captive nations," Lithuania, Latvia and Estonia. Four politicians spoke at the event. The most famous one, whose name I've nevertheless forgotten (but then he was the "star" attraction), talked about the plight of Soviet Jews, which was a bit tangential. Two others provided generic stump speeches. One guy had done his homework, and addressed the crowd as if he really knew them, and shared their very real concerns. This guy was obviously smart, hard working, and deeply respectful of his audience.

This guy was Jack Kemp.

Over the years I accompanied my wife to many small gatherings, and a few large ones, where politicians spoke. They were usually polite, cordial and clueless. Jack Kemp was different.

Here's the New York Times obit on Kemp. It gives him great credit, as it should, for advocating the Kemp-Roth tax cuts.

Here's additional background from Jeffrey Bell on the debates within the Republican party over the Kemp-Roth approach. I had not realized that this had ever been controversial. Even more, I had not realized that Congress passed a diluted version Kemp-Roth tax cuts in 1978, only to have them vetoed by President Carter! Imagine how different the world would be had Carter launched the recovery of capitalism instead of Reagan!

The Kemp-Roth tax cuts were incorporated into the Economic Recovery Tax Act, which was enacted about 20 months after I joined the Merrill Anderson Company. We did very well publishing information for trust departments to use in publicizing the big and small changes that were ushered in. (Before ERTA, a Q-TIP was a just a stick with a cotton ball on the end.) It may have been my work on communicating about ERTA that led Merrill Anderson's senior management to believe I had to potential to break out of our attorney programs.

Thank you, Jack Kemp!

Saturday, May 02, 2009

Does "Tax the Rich" Have an Upside?

Those who make over $250,000 a year (and Joe the Plumber, who doesn't) may object to the idea of raising the top income tax rate. But it's probably good news for tax accountants and financial advisers. Evidence: Reactions in the U.K. to their new top income-tax rate of 50 percent.

Subscribe to:

Comments (Atom)

{kind=link}